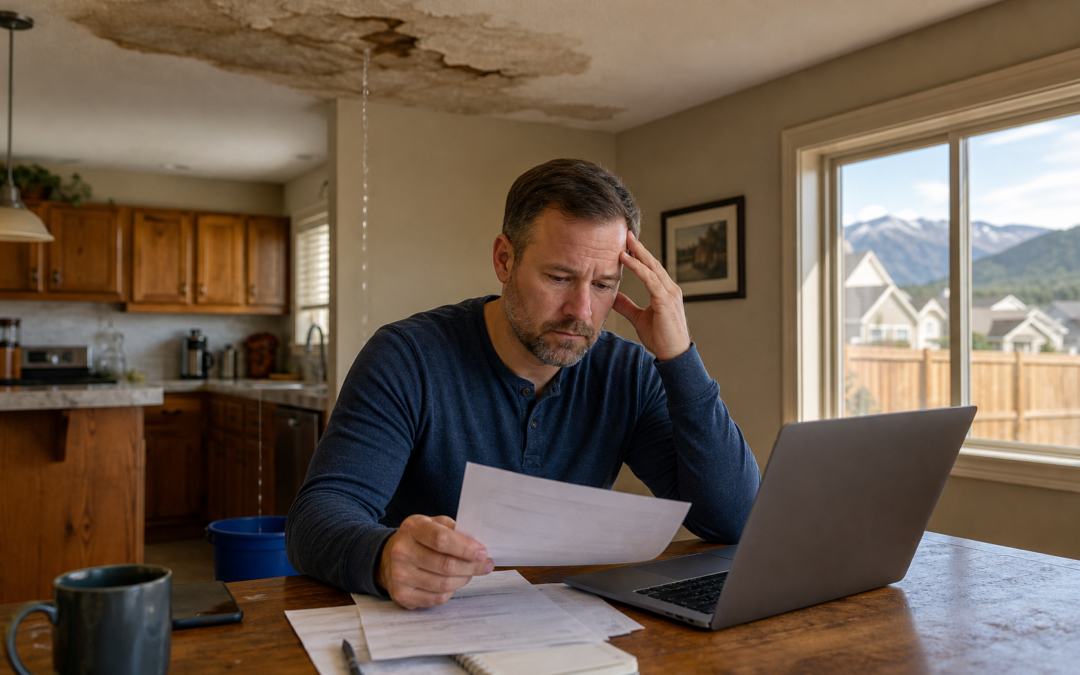

You just found standing water in your basement, a burst pipe behind the wall, or a ceiling stain that’s getting bigger by the hour. Your first thought is probably: does my insurance even cover this?

It’s one of the most common questions Northern Colorado homeowners ask — and the answer isn’t as simple as yes or no. What your homeowners policy covers depends on how the water damage happened, when you discovered it, and what you did about it. Understanding the difference before you file a claim could save you thousands of dollars and months of frustration.

Here’s the truth about water damage coverage in Colorado — and the steps you should take right now to protect your home and your claim.

What Standard Homeowners Insurance Typically Covers

Most homeowners policies in Colorado cover water damage that is sudden and accidental. That’s the key phrase your insurance adjuster is looking at.

Examples of water damage that’s usually covered:

- A pipe that bursts unexpectedly inside your walls or under your slab

- An appliance failure — your washing machine hose snaps, your dishwasher overflows, your water heater ruptures

- Sudden roof leaks caused by storm damage (hail, fallen tree limbs)

- An accidental overflow from a bathtub or toilet

- Water damage from firefighting efforts

In these cases, your standard HO-3 policy generally covers the cost of water extraction, drying, structural repairs, and damaged personal property — minus your deductible.

What Homeowners Insurance Usually Does NOT Cover

This is where most Colorado homeowners get surprised. Your standard policy almost certainly does not cover:

- Gradual leaks. If a pipe has been slowly dripping behind your wall for weeks or months, that’s considered a maintenance issue — not a sudden event. Insurance companies routinely deny these claims.

- Flooding from outside sources. Rising rivers, flash floods, storm runoff, and groundwater seeping into your basement are NOT covered by homeowners insurance. You need a separate flood insurance policy for that (more on this below).

- Sewer and drain backups. If a city sewer line backs up into your home, your standard policy likely won’t cover it unless you’ve added a specific sewer backup endorsement.

- Neglected maintenance. If the damage resulted from a roof you never repaired, a known plumbing issue you ignored, or a sump pump you didn’t maintain, your insurer can deny the claim.

The common thread? Insurance covers sudden accidents, not gradual neglect. If the insurer can argue you should have caught the problem sooner, they will.

The Three Situations Where Colorado Homeowners Get Denied

After working with hundreds of water damage situations across Northern Colorado, we see the same denial patterns over and over:

1. You waited too long to act. Even if the initial event was sudden, your insurer expects you to mitigate the damage immediately. If you discover a burst pipe on Tuesday and don’t call a restoration company until Friday, the insurer may argue the secondary damage — mold, warped floors, structural deterioration — was preventable. Time matters.

2. You filed the claim before documenting the damage properly. Your insurer needs to see what happened. If you start ripping out drywall or throwing away damaged materials before the adjuster documents them, you lose leverage on your claim. Documentation comes first.

3. You called your insurance company before calling a restoration professional. This is a big one. Your insurer’s first priority is limiting their payout. A restoration professional’s first priority is protecting your home. When you call Revive before calling your insurance carrier, we document everything, begin emergency mitigation immediately, and help you file a claim that’s backed by professional evidence. That changes the entire dynamic.

When You Need Separate Flood Insurance

If you live in Northern Colorado — especially near the Cache la Poudre River, the Big Thompson, or in any of the flood zones across Loveland, Fort Collins, Greeley, or Windsor — you should seriously consider a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private carrier.

Standard homeowners insurance does not cover:

- Flash flooding from summer thunderstorms

- River overflow and rising water tables

- Mudflow and surface water runoff

- Snowmelt flooding in spring

After the devastating floods this region has experienced, flood insurance isn’t optional for many NOCO homeowners — it’s essential. If you’re not sure whether you’re in a flood zone, your insurance agent or your local county floodplain administrator can tell you.

What to Do Right Now If You Have Water Damage

If you’re reading this because water is actively damaging your home, here’s what you need to do — in this order:

Step 1: Call Revive Restoration at (720) 340-3499. We respond within 60 minutes across Northern Colorado and begin emergency water extraction and drying immediately. This is the single most important step to protect both your home and your insurance claim.

Step 2: Document everything. Take photos and videos of all visible water damage before anything is moved, cleaned, or removed. Capture the source of the water if possible.

Step 3: Stop the water source if it’s safe to do so. Shut off the main water valve if it’s a plumbing failure. Don’t enter standing water near electrical outlets or panels.

Step 4: File your insurance claim — with Revive’s documentation backing you up. When you call your insurer with professional mitigation already underway and thorough documentation in hand, your claim is stronger from the start.

Why Calling Revive Before Your Insurance Company Matters

Here’s what most homeowners don’t realize: your insurance company does not work for you. Their adjuster’s job is to determine the minimum payout. When you call Revive first, you get an independent, professional assessment of the damage. We document the scope of loss with moisture readings, thermal imaging, and detailed photo evidence — the kind of documentation that supports your claim instead of the insurer’s bottom line.

Every hour of delay increases the damage. Mold can begin growing in as little as 24-48 hours. Structural materials weaken. Restoration costs go up. Insurance adjusters know this — and they know that homeowners who act fast and document well are harder to underpay.

The Bottom Line

Does homeowners insurance cover water damage in Colorado? Often, yes — but only if the damage was sudden, you acted quickly, and you documented everything. The single best thing you can do to protect your home and your claim is to call a professional restoration company before calling your insurance carrier.

Revive Restoration serves homeowners across Johnstown, Loveland, Windsor, Fort Collins, Greeley, and all of Northern Colorado. We’re locally owned, we respond within 60 minutes, and we work with every insurance carrier.

Call (720) 340-3499 for a free inspection — before the damage gets worse and before your claim gets complicated.